In JPMorgan crypto news, the bank, alongside Chase, Citigroup, Bank of America, and Wells Fargo, has confirmed plans to build a shared tokenized deposit network through The Clearing House, the real-time payments company they collectively own, with a target launch in the first half of 2027.

The network, operating on blockchain infrastructure, will enable instant 24/7 settlement and programmable payments while keeping every dollar inside the regulated banking system. This is the largest coordinated banking move into blockchain technology in US history and a direct response to stablecoin issuers like Tether and Circle.

Here is the central tension this article unpacks: bank-grade tokenized deposits and crypto-native stablecoins are now racing toward the same finish line, instant, programmable digital dollars, but they are built on fundamentally different foundations, serve different users, and carry different risks.

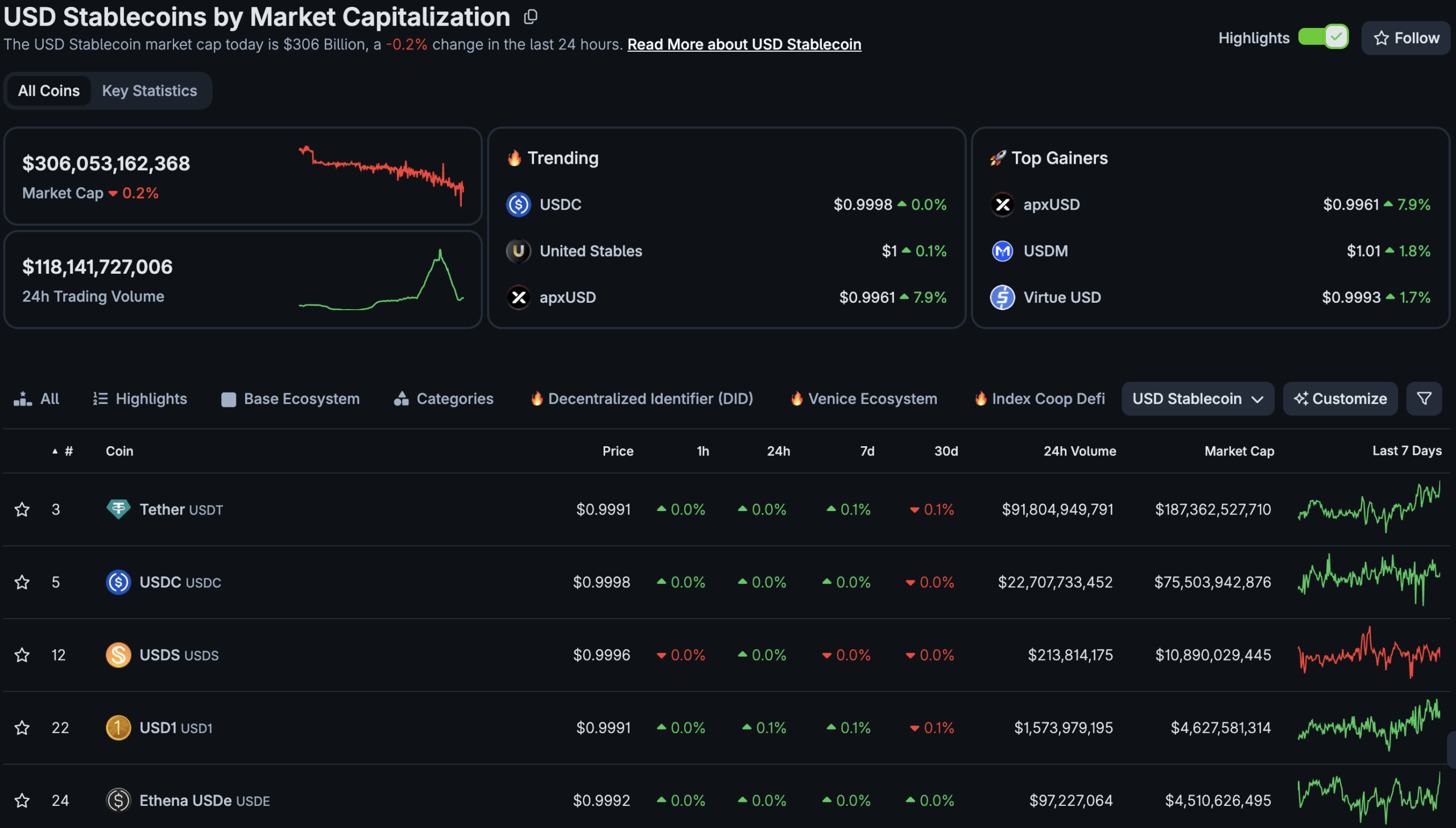

This news comes as Bitcoin sits flat on the day, just above $63,300, while the total crypto market cap has shed 2.9% in the past 24 hours, now at $2.22 trillion, down from $2.7 trillion just 10 days ago.

$BTC dropped to $61,000 again.

Sellers are in full control, and they are trying to push Bitcoin below $60,000.

Once that happens, we will see the full capitulation. pic.twitter.com/JWsFi9qOqJ

— Ted (@TedPillows) June 5, 2026

Tokenized Deposits Explained: What the Regulated Settlement Network Actually Does and Why Banks Want It

A tokenized deposit is like a digital coat-check ticket for your bank balance. You exchange your dollars for a blockchain-based token representing that amount, which can be transferred instantly to anyone in the network at any time. When cashed in, the recipient gets real bank dollars back, no crypto wallet or separate asset needed.

What it is not: a new cryptocurrency, a private stablecoin, or a Central Bank Digital Currency (CBDC). It stays within the banking system, maintaining the same credit protection and accounting treatment as funds in your checking account.

The Regulated Settlement Network connects bank payment rails to this blockchain, enabling member banks to transfer tokenized deposits instantly, a process known as atomic settlement. Citi’s Token Services already facilitates real-time transfers across major cities, serving as a model for scaling this network.

Key advantages include 24/7 settlement, programmable payments via smart contracts, and instant finality rather than pending next-business-day clearing.

DISCOVER: Best New Cryptocurrencies to Invest in 2026

JPMorgan Crypto News: What Jamie Dimon and Citi’s Blockchain Bet Actually Signals for the Financial System

JUST IN: JPMorgan, Citi and major US banks to launch new tokenized deposit system to compete with crypto.

— Watcher.Guru (@WatcherGuru) June 4, 2026

JPMorgan’s Kinexys platform has been processing institutional payments using JPM Coin on a private blockchain since 2020. In 2026, JPMorgan launched a tokenized deposit token on Base, Coinbase’s public Layer 2 network, indicating its willingness to adopt public blockchain technology. This move shows that JPMorgan views blockchain interoperability as an asset rather than a threat.

Citi’s Shahmir Khaliq emphasized that banks are not just experimenting with blockchain; they are responding to stablecoin firms taking payment and settlement business. David Watson, CEO of The Clearing House, described the initiative as a significant shift in the industry towards on-chain payments.

Not all banks share the same urgency. Bank of America’s Mark Monaco noted a lack of immediate demand for tokenized deposits but acknowledged that adoption takes time. The 2027 launch reflects a proactive approach to building infrastructure ahead of demand.

EXCLUSIVE: Earn $10 USDC Via Binance Sign-Up

Will Tokenized Deposits Replace Stablecoins? What the RSN Means for USDT and USDC

The honest answer is that tokenized deposits appeal to some users but not others. They excel in wholesale institutional settlement, making them a great fit for corporate treasurers handling large transactions, especially with their instant settlement and FDIC-equivalent protections. For instance, the JPMorgan crypto digital bank deposit could be an attractive alternative to holding USDC.

However, tokenized deposits struggle in the retail space where stablecoins like USDT and USDC thrive. These stablecoins cater to individuals without US bank accounts and those in high-inflation economies seeking dollar exposure, benefiting from their permissionless access.

Stablecoin issuers aren’t idle; companies like Circle and Tether are working to gain regulatory approvals to tap into the institutional market. The landscape is shifting with bank-backed stablecoin initiatives like SoFi USD and Ripple’s RLUSD, aiming for the same regulated dollar segment.

Bull case: Tokenized deposits and stablecoins coexist, with banks dominating institutional settlement and stablecoins thriving in DeFi and emerging markets.

Base case: By 2029, tokenized deposits will likely lead institutional interbank settlements, while USDT and USDC will maintain their retail dominance.

Bear case: Stricter stablecoin regulations could accelerate their decline in regulated markets, limiting their institutional reach faster than companies can adapt.

EXPLORE: Best Meme Coin ICOs to Invest in 2026

The post JPMorgan Crypto Revolution: Will Tokenized Deposits Kill Stablecoins? appeared first on 99Bitcoins.

{kind=link}